| Formats |

Paperback |

eBook |

| Formats |

Paperback |

eBook |

Overview

The Patient Protection and Affordable Care Act—a.k.a. Obamacare—remains highly controversial and faces ongoing legal and political challenges. Polls show that by a large margin Americans remain opposed to the healthcare law and seek to “repeal and replace” it. However, the question is: Replace it with what?

In A Better Choice, John C. Goodman clearly and concisely provides the compelling answer—no small feat, considering the complexity and intransigence of problems that have long plagued American healthcare. His prescription of four key reforms may garner the greatest attention as policymakers and the public search for a way out of the healthcare quagmire. For anyone who wants to learn about some of the boldest prescriptions designed to remedy our healthcare system, Goodman’s book is a must-read.

Contents

1. IntroductionPart I: Problems and Principles

2. Six Major Problems of the Affordable Care Act (ACA)Part II: Taking a Closer Look at the Principles

3. Six Principles for Commonsense Reform

4. Understanding ChoicePart III: Curing the Healthcare Crisis

5. Understanding Fairness

6. Understanding Universal Coverage

7. Understanding Portability

8. Understanding Patient Power

9. Understanding Real Insurance

10. Can the ACA Be Fixed?Notes

11. The Case for a Fixed-Sum Tax Credit

12. Why I Am More Egalitarian on Healthcare Than Most Liberals

Index

About the Author

Detailed Summary

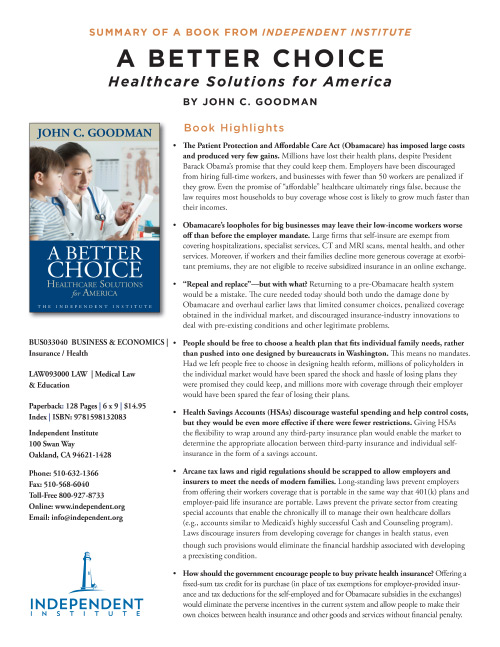

- The Patient Protection and Affordable Care Act (Obamacare) has imposed large costs and produced very few gains. Millions have lost their health plans, despite President Barack Obama’s promise that they could keep them. Employers have been discouraged from hiring full-time workers, and businesses with fewer than 50 workers are penalized if they grow. Even the promise of “affordable” healthcare ultimately rings false, because the law requires most households to buy coverage whose cost is likely to grow much faster than their incomes.

- Obamacare’s loopholes for big businesses may leave their low-income workers worse off than before the employer mandate. Large firms that self-insure are exempt from covering hospitalizations, specialist services, CT and MRI scans, mental health, and other services. Moreover, if workers and their families decline more generous coverage at exorbitant premiums, they are not eligible to receive subsidized insurance in an online exchange.

- “Repeal and replace”—but with what? Returning to a pre-Obamacare health system would be a mistake. The cure needed today should both undo the damage done by Obamacare and overhaul earlier laws that limited consumer choices, penalized coverage obtained in the individual market, and discouraged insurance-industry innovations to deal with pre-existing conditions and other legitimate problems.

- People should be free to choose a health plan that fits individual family needs, rather than pushed into one designed by bureaucrats in Washington. This means no mandates. Had we left people free to choose in designing health reform, millions of policyholders in the individual market would have been spared the shock and hassle of losing plans they were promised they could keep, and millions more with coverage through their employer would have been spared the fear of losing their plans.

- Health Savings Accounts (HSAs) discourage wasteful spending and help control costs, but they would be even more effective if there were fewer restrictions. Giving HSAs the flexibility to wrap around any third-party insurance plan would enable the market to determine the appropriate allocation between third-party insurance and individual self-insurance in the form of a savings account.

- Arcane tax laws and rigid regulations should be scrapped to allow employers and insurers to meet the needs of modern families. Long-standing laws prevent employers from offering their workers coverage that is portable in the same way that 401(k) plans and employer-paid life insurance are portable. Laws prevent the private sector from creating special accounts that enable the chronically ill to manage their own healthcare dollars (e.g., accounts similar to Medicaid’s highly successful Cash and Counseling program). Laws discourage insurers from developing coverage for changes in health status, even though such provisions would eliminate the financial hardship associated with developing a preexisting condition.

- How should the government encourage people to buy private health insurance? Offering a fixed-sum tax credit for its purchase (in place of tax exemptions for employer-provided insurance and tax deductions for the self-employed and for Obamacare subsidies in the exchanges) would eliminate the perverse incentives in the current system and allow people to make their own choices between health insurance and other goods and services without financial penalty.

Despite having surmounted numerous obstacles, the Patient Protection and Affordable Care Act (ACA)—a.k.a. “Obamacare”—remains highly controversial and faces ongoing legal and political challenges. The law’s staunchest critics are saying “repeal and replace.” Even its supporters acknowledge that serious changes are needed. The question is: replace it with what?

In A Better Choice: Healthcare Solutions for America, economist and Independent Institute Senior Fellow John C. Goodman answers the question clearly and concisely. For anyone who wants to better understand Obamacare’s most serious problems and learn about some of the boldest prescriptions designed to remedy them, Goodman’s book is a must-read.Problems and Principles

The Affordable Care Act creates numerous problems, but six are especially troubling, Goodman explains in Part I.

- It imposes an impossible mandate. The ACA requires Americans to buy a package of benefits whose cost is likely to grow faster than our incomes. That means healthcare will crowd out of the family budget more and more of other goods and services we need and want to buy. Because of an inflexible mandate, people’s ability to get off of this impossible path is greatly limited.

- It makes promises that aren’t paid for. Although the healthcare law requires us to purchase health insurance whose costs are likely to grow faster than our incomes, the subsidies provided by the government are capped and will grow at a much slower rate.

- It promises what it cannot deliver. Obamacare was supposed to insure 26 million previously uninsured people, but the supply of medical personnel cannot come anywhere close to meeting such a demand.

- Its subsidies and mandates act to destabilize entire sectors of the economy. Depending on their size, employers will face pressure to curtail hiring, rely more on part-time employees, and outsource jobs to non-employee labor. Because most workers who earn less than the average wage will be better off getting insurance in the exchange, and most who earn more than the average wage will be better off getting insurance at work, entire industries will be encouraged to reorganize in response to these incentives.

- It creates perverse incentives that threaten the quality of care. By prohibiting insurers from charging premiums that reflect a consumer’s health status, Obamacare requires them to overcharge the healthy and undercharge the sick. This creates pressures for insurers to try to attract the healthy and to avoid the sick. After enrollment, their incentive is to over-provide to the healthy and under-provide to the sick.

- Its weakly enforced mandate will undermine the health insurance marketplace. The lack of real penalties for remaining uninsured are encouraging the healthy to wait to enroll until they get sick. This creates the risk of a “death spiral,” whereby the pool of insured becomes increasingly small, unhealthy, and expensive to ensure.

These six problems could have been avoided had the architects of healthcare reform adopted six commonsense principles. They are: choice, fairness, universal coverage, portability, patient power, and real insurance.

“What would it cost to create an alternative to the ACA based on these six principles?” Goodman asks. “I believe that if we take all of the current subsidies for employer-provided insurance and add all of the subsidies the ACA is providing, there is more than enough money for the reforms I recommend.”

A Closer Look at the Principles

In Part II, Goodman elaborates on these principles by drawing on his awarding-winning, 2012, Independent Institute book, Priceless: Curing the Healthcare Crisis.

Understanding choice. Under the ACA, the health insurance benefits you must buy are determined by the government’s needs and the needs of the special interests that helped shape the health-reform law. The alternative is to let people chose the package of benefits that meet their own individual and family needs.

Understanding fairness. Most of the uninsured lack access to employer-provided health insurance purchased with pre-tax dollars. If they obtain insurance at all (and if they don’t qualify for the Obamacare tax credit), they must buy coverage with after-tax dollars, which effectively doubles the after-tax price for middle-income families. On the other hand, if they do qualify for a tax credit on the new health-insurance exchange, their subsidy may be many times greater than the tax subsidy enjoyed by people at the same income level who get coverage at work.

This unfairness could be eliminated by giving people who obtain health insurance the same tax relief whether they obtain coverage at work, in the marketplace, or in an exchange.

Understanding universal coverage. If ensuring that everyone has coverage is a worthy goal, one solution is to offer a uniform, fixed-dollar tax credit for health insurance. The credit would be refundable (even those who don’t have a federal tax liability could claim it). It would be generous enough to allow people to purchase Medicaid-like insurance, and any unclaimed tax subsidies would be sent to safety-net institutions that serve the uninsured.

Understanding portability. Lack of portability of employer-based insurance is one of the biggest problems with the U.S. healthcare system. Even coverage obtained in the Obamacare exchanges is generally not portable: People lose their eligibility for health plans purchased in an exchange (or lose their eligibility for tax-subsidized coverage) if they become eligible for Medicaid or accept a job with an employer that offers minimum essential coverage at an affordable price.

The alternative is to allow employers to do what Obamacare now forbids them to do: buy insurance that the employees own and can take with them from job to job and in and out of the labor market. By promoting long-lasting relationships between patients and healthcare providers, insurance portability would strengthen continuity of care. Also, portability is more compatible with a dynamic economy that requires job mobility.

Understanding patient power. Healthcare decisions are generally more successful when patients directly control their own health dollars and can weigh the tradeoffs between health care and other uses of money. A famous study by the RAND Corporation in the 1980s, for example, found that consumers with relatively high deductibles of around $2,500 (in today’s prices) consumed 30 percent less healthcare than those with no out- of-pocket costs, but their reduced consumption of care had no adverse health effects. Patients became more cost conscious, but they did not do things that were harmful to their health.

Understanding real insurance. Instead of trying to force insurers to take enrollees they don’t want, in a real insurance market the insurer would receive a premium that reflects the enrollee’s expected actuarial cost. That would allow insurers to compete on a level playing field for the sick and the healthy—much as they currently do in the Medicare Advantage program. What some people call “change-of-health-status insurance” would allow people to insure against the costs of developing a preexisting condition.

Curing the Healthcare Crisis

In Part III, Goodman proposes numerous recommendations to bring greater affordability, access, and quality to the U.S. healthcare system. Four reforms would be especially helpful. Although they wouldn’t correct every problem Obamacare creates, they would go a long way toward eliminating them by harmoniously aligning the incentives of patients, healthcare providers, and insurers. They consist of the following:

- Replacing all the Obamacare mandates and subsidies with a universal tax credit that is the same for everyone—preferably worth $2,500 for an adult and $8,000 for a family of four.

- Replacing all the different types of medical savings accounts with a Roth Health Savings Account (i.e., after-tax deposits and tax-free withdrawals).

- Allowing Medicaid to compete with private insurance, with everyone having the right to buy in or get out.

- Denationalizing and deregulating the ex- changes and requiring them to institute change-of-health-status insurance.

Together these four reforms would bypass the technical hurdles of the online exchanges, prevent perverse outcomes in the labor market, stop the exchanges’ “race to the bottom” (by adopting ever narrower networks), reduce the financial burden of high deductibles, and provide real protection for pre-existing conditions.

Understanding the case for a fixed-sum tax credit is especially important because lawmakers have introduced several bills offering flawed provisions for tax credits. Goodman illustrates the advantages of his approach by comparing it with proposals offered by Sen. John McCain during his 2008 presidential bid, a bill authored by Sen. Tom Coburn and Rep. Paul Ryan, and other proposals.

In his visionary final chapter, “Why I Am More Egalitarian on Healthcare Than Most Liberals,” Goodman describes how lifting various government controls in health-insurance markets would empower the least fortunate members of society.

“The result,” writes Goodman, “would be a healthcare system that would be unquestionably more equitable than what you see in either Britain or Canada and a lot more equitable than what we will experience under the Affordable Care Act.”

Praise

“Nancy Pelosi famously told us that we could find out what was in the Affordable Care Act once it passed. It is now five years later, and thanks to its convoluted concepts and its thousands of pages of rules and regulations few have wended their way through the ACA, and still fewer understand what it all means. Fortunately John Goodman, an expert on the American health system and a perceptive analyst, has studied the Act and has written the insightful book A Better Choice, that reveals what is in the ACA, what is wrong with it, and what could and should be done to provide cost-effective healthcare to our citizens. The ACA starts from the premise that the federal government knows best when it comes to the provision of healthcare. John Goodman shows the pitfalls of this premise and how the market can be harnessed to align consumer choice and provider incentives to more effectively resolve the issues of resource use and financing of healthcare. Markets are particularly important for the U.S. which has a huge and highly heterogeneous population—317 million people (third largest in the world).”

—June E. O’Neill, Wollman Distinguished Professor of Economics and Director of the Center for the Study of Business and Government, Baruch College; former Director, Congressional Budget Office

“John Goodman understands the real life effects of the Affordable Care Act and the proposed alternatives. John also writes extremely well, making complicated concepts clear. All this makes A Better Choice a highly recommended read for those who wish to understand the current health policy debate.”

—Bill Cassidy, M.D., U.S. Senator

“John Goodman has written a clear and compelling analysis of America’s health care morass. Anyone who wants to understand what the politicians and policy wonks are arguing about should turn to A Better Choice. Liberals and conservatives should both read this book to understand why Obamacare does not work as it was supposed to. Everyone should read this book to learn what the solution is.”

—Joseph R. Antos, Wilson H. Taylor Scholar in Health Care and Retirement Policy, American Enterprise Institute

“In A Better Choice, John Goodman has written an eye-opening analysis of the many problems with Obamacare and has proposed common-sense solutions.”

—Pete Sessions, Chairman, Committee on Rules, U.S. House of Representatives

“Our health care system continues to face higher costs, more mandates, and complicated rules, even as the needs of the consumer are constantly changing. America needs new and innovative approaches—‘solutions’—to chart a better course on care. Dr. Goodman has proved himself an innovator, and with his book A Better Choice, he continues to challenge policymakers with thoughtful, market-based approaches toward health care.”

—John M. Engler, former Governor of Michigan; President and CEO, Business Roundtable

“John Goodman has been one of the most important health economists in the country. He has been an informed and prescient critic of the current health system, and his forecasts of the failings of Obamacare have been exactly on target. He has also been a leader in proposing workable alternatives, and his health savings account plan has been a success whenever it has been used. In A Better Choice he continues his important work. He first shows in detail what is wrong with Obamacare. But he does not stop there: he provides the important alternative, fixed-sum tax credits, that could and should replace all other health subsidies, including the subsidy for employer provided health insurance. He shows how this plan could greatly improve the efficiency of our health care system and also lead to increased health care for the disadvantaged. This is a serious book and one the new Congress should examine very carefully.”

—Paul H. Rubin, Samuel Candler Dobbs Professor of Economics, Emory University

“A Better Choice is an intriguing book that combines John Goodman’s most sensible proposals all in one place. It directly addresses the litany of the issues we face with the two sides on the how to deal with these issues. On the one hand it contrasts the ACA vision with the reality. On the other hand it outlines how simple a real solution might be.”

—Thomas R. Saving, Jeff Montgomery Professor of Economics and Director of Private Enterprise Research Center, Texas A & M University

“In A Better Choice, John Goodman has worked a miracle. He has distilled the essence of a plan to improve the limping and vulnerable Obamacare program into four points (read the book to find out), which improve opportunities for choice, improve efficiency in that choice, and expand the set of people likely to end up with health insurance coverage. Not that everyone, on either left or right, will agree with all of the particulars of each point or their suggested implementation—but the book does provide a fresh starting point, an alternative narrative, that is virtually guaranteed to get us to a better place than we are at present.”

—Mark V. Pauly, Bendheim Professor, Professor of Health Care Management, and Professor of Business and Public Policy Wharton School; University of Pennsylvania; former Commissioner, Physician Payment Review Commission

“Regardless of whether the Affordable Care Act (ACA) has any merit in theory, its practical realities point toward a death spiral as it will likely collapse under its own weight, for all the reasons John Goodman lucidly recounts in A Better Choice. Goodman offers a thoughtful, thought-provoking alternative to the ACA (Obamacare) and the enormous harms it would cause, to which everyone, especially all those who favor free markets and limited government, should pay very close attention.”

—E. Haavi Morreim, Professor, College of Medicine, University of Tennessee Health Science Center

“One good thing that has come out of the Affordable Care Act is that it has produced serious debate about how to fix the American healthcare system. An excellent place for readers interested in this question to start would be John C. Goodman’s A Better Choice, which zeroes in on the many problems with the ACA and proposes workable, market-based alternatives.”

—Joel M. Zinberg, M.D., J.D., F.A.C.S., Associate Clinical Professor, Icahn School of Medicine at Mount Sinai Hospital; Visiting Scholar, American Enterprise Institute

—Robert F. Graboyes, Senior Research Fellow, Mercatus Center, George Mason University

“After half a decade of turmoil generated by the Affordable Care Act in a three trillion dollar healthcare economy, John Goodman’s A Better Choice succinctly diagnoses the problems and lays out a practical treatment plan. His six principles of health reform transcend the poisoned and dishonesty of late and offer the proper terms for a real solution. As politicians search to find remedies before the health economy is too damaged to alter course, they will be well served reading and acting on the policy prescriptions in A Better Choice.”

—Stephen T. Parente, Minnesota Insurance Industry Chair of Health Finance, Associate Dean of MBA Programs, and Director of the Medical Industry Leadership Institute; Carlson School of Management; University of Minnesota

“The Affordable Care Act signed into law by President Obama abruptly altered the pathway of healthcare in the U.S. Contrary to the desire of most Americans, this government centralization was undertaken without understanding, or perhaps even in spite of, the deleterious impact it would have on medical care access, quality, and cost, and without regard for its broader harms to employment and future healthcare innovation. In A Better Choice, John Goodman articulates the important problems with Obamacare in clear language, laying out the core impacts of the law for all those interested in truly understanding the issues. He then details how to transition to a healthcare system that provides access to all while maintaining the high quality of what is factually the world’s best medical care. I highly recommend the book to all those interested in the future of America’s health care.”

—Scott W. Atlas, David and Joan Traitel Senior Fellow, Hoover Institution, Stanford University

“As Obamacare continues to present us with more complications and disappointments, A Better Choice indeed offers in clear and compelling terms, a better choice for all Americans—one that strips away the bureaucratic controls and mandates, and allows consumers to take over their own healthcare decisions. John Goodman provides a devastating indictment of the current system, and supplies a clear roadmap toward a more certain and prosperous future.”

—Richard A. Epstein, Laurence A. Tisch Professor of Law, New York University

“If you think that the Patient Protection and Affordable Care Act (ACA, also known as Obamacare) is bad because of its expense, the distortions it causes in the labor market, its failure to provide people what they really want, and its highly unequal treatment of people in similar situations, wait until you read John C. Goodman’s A Better Choice: Healthcare Solutions for America. You will likely conclude that the ACA is even worse than you thought. That’s the bad news. The good news is that Goodman, a health economist and senior fellow with the Independent Institute, proposes reforms that would do more for the uninsured than the ACA does, and at lower cost, and also would make things better for the currently insured. And it would do all this while avoiding mandates, creating more real competition among insurers, and making the health care sector more responsive to consumers. . . . Goodman is strongest on the issue on which he has always been strong: patient power. . . . Goodman points out that if patients were spending their own money, other parts of the health care system would respond by making things more consumer-friendly. Will we see any of the policy changes that Goodman proposes? Time will tell.”

—Regulation